This is an unedited version of my

Sunday Times article from March 16, 2014

To those who lived through the tropical storms annually ravaging the Southern Atlantic coast of the US, calm is not always the tranquility beyond the storm. Often, it is the tranquility in the eye of a hurricane.

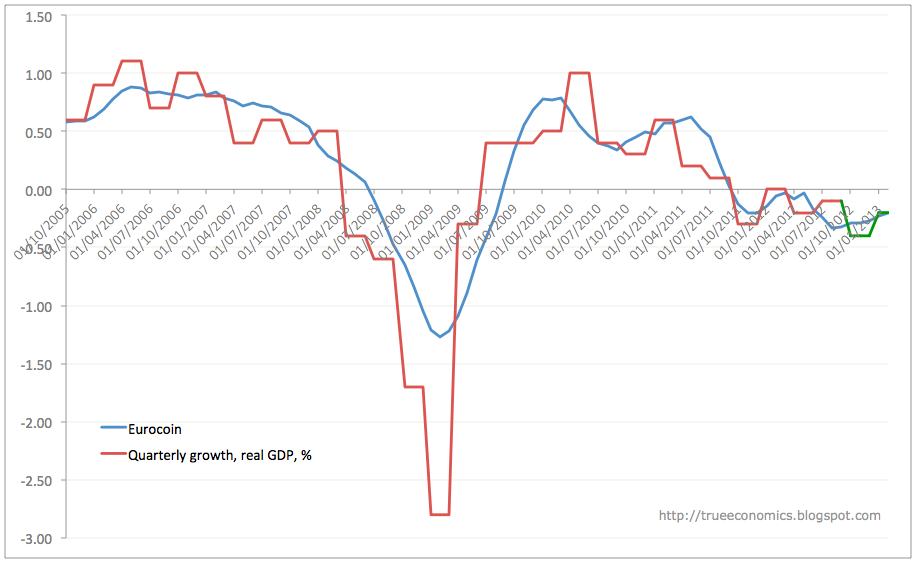

The current state of economic affairs in Ireland, the sunshine washing across the markets, the warm-ish glow of a recovery, the steady diminishment of the crisis rhetoric - all are the sign of a fragile state of affairs brought about by the extraordinary monetary policies of the ECB since the beginning of 2012. As such, the change in economic weather we have experienced to-date can be a temporary respite rather than a permanent rebound.

In October 2012, three months after declaring that the ECB will do whatever it takes to save the euro, Mario Draghi noted another worrying regularity - the problem of differential pricing of debt across the euro area. At first, he was referencing government debt markets. Later, he started to show concern for the same trends emerging in all credit markets, including those for corporate debt.

Ever since then, the ECB has signalled that the Central Bank's core policy in dealing with the crisis will remain accommodative. Historically low policy rates, the promises of the Outright Monetary Transactions and the structuring of the Banking Union – together constituting what is known as the Draghi Put – were the Frankfurt's attempts to break down the fragmentation across various euro area economies. These measures were successful in reducing the differences in sovereign bonds yields between the euro area member states. First Ireland, Italy and Spain, then Portugal and Greece, all peripheral countries have seen their bond spreads over the German benchmark 10 year bunds come down dramatically in the course of the last 20 months.

Since mid-2012, therefore, the Draghi 'Put' underwrote historically low policy rates. It is this 'Put' that has been credited by the researchers at the ECB and the IMF, as well as by a number of academics, as the main driver behind the decline in euro area peripheral countries cost of borrowing, saving Irish taxpayers billions in interest on Government debt, helping hundreds of thousands of Irish borrowers to lower tracker mortgages costs and supporting our exit from the Troika programme.

But, in effect, the Draghi Put has also thrown a veil of ignorance over the core problems still working through the euro area economies: problems of excessive legacy debts, lack of structural drivers for the recovery and the transfer of public and banking debts onto the households' balance sheets through fiscal austerity. ‘Whatever it takes' monetary policies might have been effective in alleviating the immediate pressures on European governments, but they did not cure the underlying disease.

In effect, the Draghi Put is not a solution to the crisis, but a potential problem of its own. It is a cure that is risking making the disease stronger.

Draghi Put has forced ECB rates (and with them the rates charged in the inter-banks markets) down to their historical lows.

Current repo rate, the main rate set by the ECB, is at 0.25 percent - the lowest since the ECB records began in January 1999. Over the period prior to the crisis, the already low (by individual nations' standards) ECB rates averaged 3.1 percent. And the duration of the ECB rates deviation from their historical norm is unprecedented: 62 months and counting. Prior to the current crisis, the longest period over which ECB rates deviated by more than 0.5 percent from their norm was 38 months. That happened in the period that created a massive financial bubble across the euro area – January 2003 through June 2006.

In general, the longer the rates rest below their long-term trend, and the further they deviate from the trend, the faster they tend to rise back toward trend levels. Exception to this norm is Japan, but hardly anyone would argue that Japanese scenario is even remotely desirable.

In simple terms, the current environment of historically low interest rates is not going to last forever. Indeed, it is unlikely to last for as long as the rates have been depressed to-date.

Alongside the above facts, there two more notable observations worth making. Darghi Put has led to a significant decline in the inter-bank lending rates. For example, Euribor 12 months contract rate has declined from the crisis-period average of 2.1 percent for the period prior to the Draghi Put to the average of 0.6 percent since July 2012. Similarly, there was a massive decline in the margin charged in the interbank markets relative to the ECB repo rate. At the same time, retail interest rates charged on new loans for Irish households and non-financial corporations have shut straight up to historical highs, when compared against the ECB policy rates. Ditto for the rates charged on existent loans.

All of this leaves our economy vulnerable to any normalisation in the interest rates policy.

Should Signore Draghi start reversing the policy rate, while Irish banks remain dependent on high lending margins to rebuild their balance sheets, Irish SMEs will face significant increase on the cost of financing their legacy loans, including the very same troubled loans that relate to property investments. Beyond triggering potential arrears and cost saving measures by the SMEs (involving layoffs), this will put strain on any growth in the SMEs sector. Capital investment costs will go up. Credit risk ratings will go down. Investment in the economy will be under severe pressure relative to the already exceptionally low rates.

Households currently working their way through arrears resolution process are likely to face high risk of relapsing into arrears. To-date, some three quarters of all restructuring deals done by the banks involve either temporary arrangements or ‘permanent’ deals that involve increases in debt carried by the households. They will face increases in the cost of restructured mortgages, impacting not only those on variable rate (the segment of the mortgage holders already heavily hit by the banks), but also trackers. Depending on how fast and at what time in the recovery process rates increases occur, the effect can be devastating. Households that are not in trouble with their lenders today will face a major hit on their incomes, depressing once again their consumption and investment and triggering a renewed bout of precautionary savings.

Counting existent loans alone, reversion to historical averages in ECB rates can take some EUR5.7 billion annually out of the real economy in higher interest costs. This would be roughly equivalent to a loss of double the annual contribution to our GDP by the Agriculture, Forestry and Fishing sector.

The above factors can also pose a threat to the Exchequer in form of lower VAT, income tax, stamps and excise receipts, exacerbated by the potential increase in the cost of borrowing that goes hand-in-hand with higher policy rates.

The good news is that given Mr Draghi's current pronouncements, we are still months, or even years, away from higher interest rates. Better news, yet, Mr Draghi has communicated that he will provide 'forward guidance' on rates policy. This commits the ECB to supplying in advance clear signals as to its intentions. Even better news is that last week Mario Draghi clearly identified output gap (the shortfall in current economic growth relative to long-term potential rates of growth) as one of the parameters watched by the ECB. This strongly suggests that Frankfurt is likely to take into consideration structurally weak economic conditions prevailing across the euro area in setting its policy rates. Such a consideration further extends the period over which low rates are likely to remain in place.

The bad news is that the only way the rates can remain low is if the euro area core remains mired in a near-deflationary Japanese economic growth scenario.

In other words, we have a choice: either the economy remains in the doldrums, unemployment stays high and incomes growth remains subdued; or the rates will go up.

Mr. Draghi Put is not based on the smaller peripheral economies conditions, but on France, Italy, Spain, Belgium, Finland and Austria as drivers of credit demand and low interest rates, and Germany as a break on low interest rates. Meanwhile, German lending constraints for non-financial companies have been at record lows for months now. There is a glut of credit in the euro area's largest economy. Thus, Germany will be ripe for rates hikes, as soon as inflation pressure picks up even moderately. The countries with shortages of credit supply are seeing their economies gradually pulling out of a recession. One can relatively safely assume that, barring new shocks, by the end of 2015 the ECB will start contemplating the end of Mr Draghi's Put.

Put conservatively, anyone with business loans or mortgages of duration greater than 5 years should be concerned. By last Central Bank of Ireland count, these loans amounted to 65 percent of all loans outstanding in the economy.

There is little we, in Ireland, can do about the direction of the ECB interest rates or the timing and the speed at which the rates increases will happen. About the only two things in our power are to ensure that current process of restructuring of SMEs loans and household mortgages is robust enough to withstand the shock of higher interest rates in the future, and that our households incomes retain the necessary cushion to absorb such increases. The former requires much more through and independently verified restructuring of our legacy debts. The latter requires lower tax burden, deep reforms and faster economic growth anchored in our real economy, not in the tax optimising MNCs-led sectors.

Absent these measures, Irish economy is a weak athlete swimming into a storm surge. The eye of the hurricane might make us feel better about our perceived strengths, but the clouds on the ECB’s horizon, no matter how distant, warn of a possible storm to come.

Box-out:

ESRI’s latest research paper on the impact of the banking sector competition on credit availability to the SMEs across the EU sheds some light on the urgency for Ireland to abandon the banking sector policy based on the Twin Pillars model. “Does Bank Market Power Affect SME Financing Constraints?” published in an influential Journal of Banking & Finance argues that banking sector retrenchment across the Eurozone towards domestic markets and reduced competition between the banks “will lead to an increase in financing constraints for SMEs”. Such constraints “will inevitably lead to lower investment and potential output. “ According to authors, “the structure of the banking system has changed dramatically following crisis... This has substantially lessened competition for business credit in Ireland with only three main retail business banks remaining. This reduction in competition poses serious questions regarding the ability of the financial system to transmit credit to SME borrowers in a recovery scenario.” In short, given Irish SMEs’ heavy reliance on bank financing, we need more than a new pillar bank. We need a fully competitive financial system operating across the economy. This will be hard to deliver on. Irish Pillar banks continue to rely on state protection for even trivial market considerations, such as deposits rates setting by their competitors, e.g. An Post. And our regulators and policymakers are still clinging to the erroneous belief that competition in the banking sector in 2001-2007 has fuelled the boom and caused the crisis.